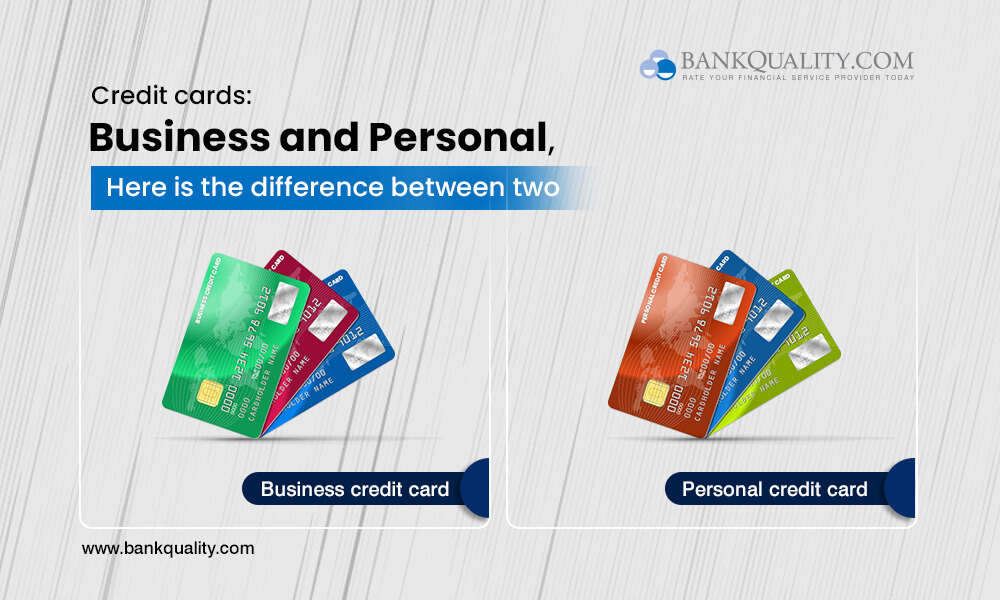

The difference between personal and small business credit cards

Navigating the world of credit cards can be overwhelming, especially when trying to differentiate between personal and small business credit cards. Both types of cards have their unique features and benefits, but knowing the key differences is crucial for managing your finances effectively. In this in-depth article, we’ll explore the distinctions between personal and small business credit cards, including their benefits, rewards programs, and credit reporting practices, to help you make an informed decision about which card is right for you.

Understanding Personal Credit Cards: Designed for Everyday Consumers

Personal credit cards are specifically designed for individual consumers and their everyday expenses. These cards often come with a variety of perks, such as cashback rewards, travel miles, and introductory offers with low or zero interest rates. They also help consumers build credit history, which is essential for obtaining loans, mortgages, and other forms of credit.

One of the primary advantages of personal credit cards is the protection they offer. Under the Credit Card Accountability Responsibility and Disclosure (CARD) Act of 2009, consumers enjoy numerous protections, such as a cap on late fees, limitations on interest rate increases, and mandatory grace periods.

Diving into Small Business Credit Cards: Tailored for Entrepreneurs

Small business credit cards are designed to cater to the needs of entrepreneurs and small business owners. They help separate personal and business expenses, which is essential for accurate bookkeeping and tax purposes. Small business credit cards also offer benefits that align with business-specific needs, such as higher credit limits, discounts on business-related purchases, and reward points for office supplies, travel, and advertising expenses.

While small business credit cards don’t come under the CARD Act, many issuers voluntarily extend similar protections to their business cardholders. Additionally, business credit cards often provide additional features like employee cards, expense management tools, and detailed spending reports, making it easier for business owners to manage their finances.

Comparing Rewards Programs: Maximizing Benefits for Personal and Business Expenses

Both personal and small business credit cards offer rewards programs, but the nature of these rewards often differs. Personal credit card rewards focus on consumer-oriented purchases, such as dining, groceries, and entertainment. On the other hand, small business credit card rewards target expenses commonly associated with running a business, like office supplies, shipping, and travel.

When selecting a credit card, it’s essential to evaluate the rewards program and choose one that aligns with your spending habits to maximize the benefits.

Credit Reporting: Personal and Business Credit Histories

Another critical difference between personal and small business credit cards lies in their credit reporting. Personal credit cards report to consumer credit bureaus, impacting the cardholder’s personal credit score. In contrast, small business credit cards typically report to business credit bureaus, affecting the business’s credit profile.

However, some business credit card issuers may also report to consumer credit bureaus, especially in cases of delinquency or default. It’s crucial to understand the reporting practices of your card issuer to ensure you maintain a healthy credit profile for both your personal and business finances.

Conclusion: Making the Right Choice for Your Financial Needs

Understanding the differences between personal and small business credit cards is crucial for managing your finances effectively. While personal credit cards cater to everyday consumers, offering consumer-oriented rewards and robust protections, small business credit cards provide entrepreneurs with tools to manage business expenses, track spending, and earn business-specific rewards.

Before deciding on a credit card, evaluate your financial needs, spending habits, and the card’s terms, rewards program, and credit reporting practices. By taking the time to analyze these factors, you can make an informed decision that best suits your personal or business financial goals.

In summary, keep these key differences in mind when choosing between personal and small business credit cards:

- Purpose: Personal credit cards are designed for individual consumers, while small business credit cards cater to entrepreneurs and business owners.

- Benefits and Rewards: Personal credit cards offer consumer-oriented rewards, while small business credit cards provide business-specific rewards and features like employee cards and expense management tools.

- Credit Reporting: Personal credit cards impact your personal credit score, while small business credit cards typically affect your business credit profile.

- Protections: Personal credit cards are protected under the CARD Act, while small business credit cards may only have voluntary protections offered by the issuer.

By considering these differences and carefully evaluating the features of each card, you can select the right credit card for your personal or business financial needs. Whether you’re an everyday consumer or a dedicated entrepreneur, understanding the nuances between personal and small business credit cards will enable you to make the most of your credit card experience and optimize your financial management strategy.

Responses